In today’s global economy, it is more important than ever for multinational companies to understand the impact domestic and foreign transactions may have on their tax accounting.

This blog was written to help you to better understand one facet of that task: tax accounting for investment in domestic and foreign subsidiaries. There are many details that you need to consider in order to provide transparency into these investments. Here I will cover three sections – inside basis vs. outside-basis, bottom-up approach, and permanent reinvestment assertion.

Inside-Basis vs. Outside-Basis

or liability and its tax basis, as determined by reference to the relevant tax laws in each tax jurisdiction. There are two categories of basis differences: “inside” basis differences and “outside” basis differences.

Inside-basis difference: difference between financial statement carrying amounts and tax basis of subsidiary’s assets and liabilities

Outside-basis difference: difference between financial statement carrying amounts and tax basis of the parent’s investment in another entity’s stock

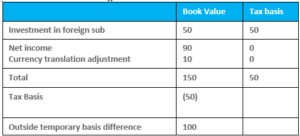

Example 1: Outside book-tax basis difference

The table below shows the difference between book and tax basis

Outside differences may result from:

- Undistributed earnings

- Foreign currency translation gain or losses included in equity

- Purchase accounting

- Impairments

- Book versus tax difference in capitalized cost

FASB Accounting Standards Codification® 740-10-25, Income Taxes, requires entities to recognize a deferred tax liability or asset for the estimated future tax effects attributable to temporary differences and carryforwards, with limited exceptions. One of these exceptions applies to the excess amount of financial reporting over the tax basis of an investment in a foreign subsidiary or a foreign corporate joint venture that is permanent in duration (i.e., permanent reinvestment assertion).

Because the exception to the requirement to provide a deferred tax liability applies only to certain investments in foreign and domestic subsidiaries, a company must first determine which entities qualify for the exception. That assessment is made using a bottom-up approach by reviewing the relationship with the investee’s immediate investor.

Bottom-Up Approach

A bottom-up approach is just what it sounds like — start from the bottom of the organizational chart and move up. There are several steps you will need to take:

1. Determine legal form of subsidiary. The nature of the legal entity matters when applying deferred tax recognition exceptions:

-

- Corporations: If controlled, there is a possibility for permanent reinvestment of the earnings.

- Partnerships: Generally, partnership earnings flow to parent for tax purposes, so permanent reinvestment would not be applicable.

- Flow-Through Entities: All items flow to parent for tax purposes, so no outside basis.

- Joint Ventures: Due to the lack of control, entities may not be able to prevent taxable repatriations/events. As a result, permanent reinvestment can generally not be asserted.

- You may need to consider ability to realize corresponding deferred tax assets, for example, US dual consolidated loss rules and foreign tax credit limitations.

- You will also need to recognize outside basis differences in:

- Cost method investments

- Equity method investments

- Partnerships

- Other flow-through entities

2. Determine domestic versus foreign relationship. The rules that determine whether a deferred tax is required depends on whether the relationship is domestic or foreign.

- The determination of whether an investee qualifies as a domestic or foreign subsidiary is made based on the relationship between the parent company and its subsidiary.

- Domestic Example: parent company is Swiss and the subsidiary is Swiss

- Foreign Example: parent company is Swiss and the subsidiary is Spanish

3. Determine tax and book basis of investment parent has in subsidiary. This step requires a substantial time commitment. You will have to take time to collect supporting documentation before making the calculations. (Note: In reality, many tax and accounting departments are not proactive in preparing tax and GAAP basis calculations. The process can be and should be automated and incorporated as a mandatory step in the year-end tax provision.

- Determine whether basis difference results in a deferred tax asset or liability

4. Review whether an exception applies to recognize Deferred Tax Assets (DTA) or Deferred Tax Liabilities (DTL)

DTA Exception

- No DTA unless basis difference will reverse in foreseeable future

- Changes in assumptions recorded as discrete events in the period that the assumption and/or underlying event occurs

DTA Exception

- Applies only to more than 50% owned domestic subsidiary (not domestic corporate joint venture)

- No DTL recognized if:

- Tax law provides means to recover investment tax free; and

- Management asserts that they expect to use the tax free recovery provision

DTA Exception – Foreign Subsidiaries and Foreign Corporate Joint Ventures

- ASC 740-30 establishes a presumption that all undistributed earnings will be transferred to the parent

- Applies only to foreign subsidiaries and foreign corporate joint ventures

- No DTL recognized if:

- Permanently reinvested

- Management’s intention and ability to indefinitely reinvest its foreign earnings Tax law provides means to recover investment tax free

Permanent Reinvestment Assertion

A company may not be required to set-up a DTL if it can demonstrate that its foreign earnings are permanently reinvested. In that regard, a company must attest to management’s intention and ability to indefinitely reinvest its foreign earnings. This is known as permanent (or indefinite) reinvestment assertion.

Permanent reinvestment assertion requires substantial quantitative and qualitative analysis (it is not an “election”). The assertion can designate which earnings are and which are not permanently reinvested on:

- An entity-by-entity determination

- A regional determination

- Certain amounts within an entity

Assessment considerations require two steps:

- US needs for foreign cash:

- Overall US cash flow

- Need for cash to service debt

- Are market conditions declining

- Foreign use of excess cash:

- Capital expenditure programs

- Planned acquisitions

- Debt covenants limiting dividend distributions

- Historical activities

It is an important note that the permanent reinvestment assertion decision is not made entirely by the finance or tax leaders in isolation but the decision must be vetted and in coordination with all of the company’s business functions. Once the question of management’s ability and intent is settled and documented, full disclosure of the amount of undistributed foreign earnings must be recorded in the notes of the financial statement. Also, any event that would lead to taxation of the unremitted earnings along with a reasonable estimate of the unrecorded deferred tax liability must be included in the documentation or a statement that indicates that a reasonable estimate is not applicable.

The entity’s analysis and documentation of permanent (indefinite) reinvestment plans (or evidence of tax-free liquidation) should generally include the following:

- Documentation supporting projected working capital and long-term capital needs in the location where earnings are generated (or other foreign locations)

- An analysis of why those funds are not needed upstream

- Consideration of current market conditions

Other documents that might be included are a management representation letter, internal control considerations, a walkthrough of the evaluation, and control testing.

Ask the Right Questions

I hope this blog gives you a better understanding of the steps to take when performing tax accounting for domestic and foreign subsidiaries. If you have additional questions, drop me an email at rwynman@gtmtax.com, or visit our International Tax page for more information.