To say that 2020 has been a challenging year is an understatement – to put it mildly. In times like these, it is good to take solace in the familiar: the fall leaves changing, turkey on Thanksgiving and, like clockwork, the uncertain fate of Section 954(c)(6). To that end we are republishing our blog post from last year on the possible expiration of Section 954(c)(6) with some slight modifications.

We also note a potential issue on the horizon for taxpayers relying on downward attribution (after the repeal of Sec. 958(b)(4) by the TCJA) to qualify for 954(c)(6). Proposed regulations issued in 2020 would disregard constructive ownership under Section 318(a)(3) in determining whether a foreign corporation is a CFC for Section 954(c)(6) purposes.[1] In an inbound context, this would mean that payments made to foreign subsidiaries owned directly/indirectly by the U.S. from other members of the group not owned under the U.S. may create Subpart F income. Proposed applicability is for taxable years ending on or after September 21, 2020, so this provision is possibly moot over the long term if Section 954(c)(6) is not extended. However, tax year 2020 could be impacted in the short term.

Much has changed since Section 954(c)(6) was enacted in 2005 and getting reacquainted with related party foreign personal holding company income (“FPHCI”) (e.g., dividends, interest, rents and royalties) and the associated calculations will take some time. While calculating subpart F is not new and taxpayers most likely had foreign base company income of another flavor over the past decade, the possible volume of FPHCI items and additional computational hoops post-TCJA mean that companies must start thinking about the expiration of Section 954(c)(6) sooner rather than later. While certainly not exhaustive, the following steps provide a thumbnail sketch of what to start considering.

Step 1: Group Related Party FPHCI and Apply Exceptions

Companies must first figure out what FPHCI payments they have. While this step may seem obvious and straightforward, most taxpayers have gotten used to look-through; consequently, the actual inventory of related party payments that may cause subpart F post-Section 954(c)(6) has probably not been tracked. It is true that intercompany information is gathered in some fashion for Form 5471, Schedule M reporting if nothing else. After all, the IRS uses this information as a subpart F litmus test of sorts when conducting an audit. Unfortunately, however, Schedule M information, typically collected through a query of the trial balance, only tells part of the subpart F story without additional analysis. After more than a decade of Section 954(c)(6), the default answer for new intercompany payments is typically that they do not create subpart F income, creating a spider’s web of FPHCI that companies have mapped at a superficial level, ignoring key details necessary to evaluate whether a payment is subpart F and what the implications are if it is.

This point is especially true if, for example, companies embraced offshore cash pooling or started charging royalties between CFCs due to supply chain changes or transfer pricing pressure from tax authorities. In other words, there is a bridge necessary to get from 5471 reporting to Subpart F and the related foreign tax credit. It is time to view these payments through a different lens. Specifically, they should be organized to determine the recipients, payors, and what payments can be removed from FPHCI due to an exception like de minimis or same country. Conversely, the full inclusion rule[1] may convert all the CFC’s income to subpart F. After the universe of FPHCI payments is aggregated, it is time to figure out what it means given the tax landscape in 2021.[2]

The TCJA has made the calculation of net subpart F, Section 78 gross up, and the foreign tax credit much more time consuming than it was. Taxpayers need to delve into the mechanics of Treas. Reg. § 1.951-1(c).[1]

Allocating and apportioning CFC deductions between the different categories of a CFC’s income (e.g., subpart F, tested income) was a much easier proposition before the TCJA and the addition of tested income. All of the above is done by treating the CFC as a domestic corporation.[2] It is also necessary to get (re)familiarized with the look-through rules of Section 904,[3] including the possible application of the often-overlooked related person interest first rule of Treas. Reg. § 1.904-5(c)(2)(ii). The net subpart F calculation and basketing determinations are littered with other nuances, some of which are not relevant without FPHCI and did not exist prior to 2006. For example, Section 951A(c)(2)(B)(ii) provides that a tested loss increases the earnings and profits (“E&P”) of a CFC in determining the E&P limitation under Section 952.[4]

To properly determine the creditable foreign taxes and related Section 78 gross up, it is necessary to apply Section 960. Section 960, which provides for an indirect foreign tax credit on subpart F income, was modified by the TCJA and now assigns foreign taxes to income if they are “properly attributable to” that income. These mechanics take on additional complexity when FPHCI is part of a CFC’s income. Generally, the final regulations require assigning taxes based on each item of FPHCI, as well as tested income and other income categories that the CFC may have (treaty basket, for example).[5] The Section 960 regulations are, in and of themselves, a heavy lift. This exercise is much more challenging than if a CFC has just tested income.

Determining the Subpart F inclusion and Section 78 gross-up does not end the quantification exercise, as it is necessary to assess the foreign tax credit limitation. Having Subpart F income can can alter the application of Section 861 when it comes to allocating and apportioning deductions for purposes of the limitation. Interest expense is typically the biggest expense, and the apportionment ration by basket will almost certainly change with Subpart F income under either the modified gross income or asset methods [6] . The prior year percentages are often used for provision and estimate purposes until they are updated later in the tax year or when the return is filed. This approach could be wrong in a material way depending on how much subpart F income exists. Even the choice of which of these methods to use should be evaluated if there is subpart F in the system.

None of the above can be accomplished without modeling. The technical rules in place are a mix of old and new; the intersection of these rules is often far from clear, and even a cursory approach often does not do justice to the results.

Step 3: Analyze the Results

If there is subpart F income, it is time to decide if that subpart F should be mitigated through check the box elections, capitalizing debt, etc. The knee-jerk reaction is, of course, that subpart F should be mitigated. The options do require scrutiny, however. For example, converting regarded payments to disregarded payments by making check the box elections, a simple enough exercise, may cause issues with stranded QBAI or taxes. These considerations did not exist prior to the enactment of Section 954(c)(6).

It is also worth remembering that with the enactment of the GILTI regime, subpart F may not be such a bad thing. Foreign base company income is removed from tested income[1] and any excess foreign tax credits arising from the subpart F income are eligible for carryback or carryforward.[2] Excess GILTI basket taxes, on the other hand, are lost.[3] The best answer might be doing nothing at all.

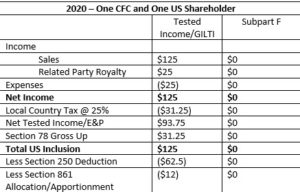

The following simplified example can help illustrate this point. For the sake of simplicity, it is assumed that the GILTI inclusion percentage[4] is 100% and the Section 250 deduction is not limited by the taxable income limitation of Section 250(a)(2).

The example below illustrates the results with the expiration of Section 954(c)(6). Again, to simplify the example, it is assumed that expenses and foreign taxes are split between tested income/GILTI and subpart F based on gross income.

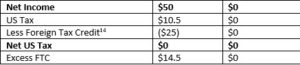

Even with simplifying assumptions, this example illustrates that the inclusion of subpart F does several things. First, it requires recomputing tested income in 2021 due to the removal of the royalty income from tested income. This removal then changes the expense allocation in determining net tested income and subpart F income at the CFC level. Second, the Section 861 results in computing the Section 904 limitation are also different. This example is very straightforward, and the reality is that the Section 861 results will likely not change pro rata due to the stock basis rules in the Section 861 regulations. The point is that an additional computational step must be completed when subpart F is part of the CFC’s income. Most importantly, the excess subpart F foreign tax credits in 2021 are valuable assets that can be carried back or forward.

The subpart F income in the example is a royalty. If the payment is interest, the analysis becomes more complicated when the US shareholder’s specified interest expense is considered. As a reminder, specified interest expense is the excess of the US shareholder’s aggregate tested interest expense over aggregate tested interest income.[1] Generally, tested interest expense and tested interest income are interest expense and income, respectively, considered in determining tested income.[2] Because some of the interest income at the recipient CFC is not tested interest income (since it is subpart F and excluded from the definition of gross tested income,) the treatment of some of the interest as subpart F could create or increase specified interest expense. As a result, the US shareholder’s 10% QBAI return could decrease.[3]

The reduction of the US corporate tax rate to 21% also makes the high tax exception (“HTE”)[4] much easier to satisfy at 18.9% — at least in theory. In practice, the HTE mechanics can be challenging given the repeal of tax pools and the new grouping and subgrouping of income and related foreign taxes for purposes of Section 960. Since the prior pooling concept is gone and the effective tax rate is determined on each type of FPHCI, the 18.9% rate, while low, may often be missed. The proposed subpart F high tax exception may further complicate these mechanics by bringing the tested unit concept (rather than item by item calculation), adjustments for disregarded payments, and coordination with the GILTI HTE, among other nuances, into play.[5] Still, given the opportunity to convert subpart F income to possibly Section 245A income it is worthwhile to run the HTE traps. Returning to the example above, the royalty income is indeed eligible for the HTE (the ETR is 25%). Such an election converts the royalty income to income eligible for Section 245A, which may be the most ideal scenario of all.

Conclusion

The expiration of Section 954(c)(6) creates additional work for companies as we move into 2021. The information needed to calculate the effect of Section 954(c)(6) expiring should be available. How quickly it can be repurposed to determine FPHCI, however, is another question. Section 954(c)(6) has become so commonplace that models with even the basic mechanics of calculating net subpart F may no longer exist or will not reflect the addition of GILTI, not to mention the need for a robust foreign tax credit calculation. Early in the calendar year, companies may be inclined to use a SALY (Same As Last Year)-type approach with respect to GILTI and the foreign tax credit as they forecast their 2021 ETR or prepare for the Q1 provision. There is risk that this approach for 2021 may be inaccurate given how increased subpart F knocks over so many dominos. The universe of related party payments, availability of exceptions, and quantification of the tax results post-TCJA require companies to start anticipating life without the look through exception. Preparing for the 2020 year-end provides an excellent opportunity to at least start this exercise.

[1] Treas. Reg. § 1.951A-1(c)(3)(iii).

[2] See Treas. Reg. § 1.951A-4(b)(1) and -4(b)(2).

[3] I.R.C. § 951A(b)(2).

[4] See I.R.C. § 954(b)(4) and Treas. Reg. § 1.951A-1(c)(3)(i)(B).

[5] See REG–127732–19, July 23, 2020.

[1] I.R.C. § 951A(c)(2). Note that dividend income is already excluded from tested income so if a CFC has dividend FPHCI the tested income calculation should generally by the same as currently. See I.R.C. § 951A(c)(2)(A)(i)(IV).

[2] I.R.C. § 904(c).

[3] Id.

[4] The inclusion percentage is corporation’s GILTI divided by tested income. I.R.C. § 960(d)(2). In other words, for purposes of this example the CFC has no qualified business asset investment (“QBAI”) and there are no CFCs with tested losses.

[1] Treas. Reg. § 1.951-1(c) has a whole host of computational rules.

[2] Treas. Reg. § 1.952-2(a)(1). Since the final GILTI regulations apply the same principle for tested income, hopefully this exercise is more familiar to taxpayers.

[3] These rules, generally, provide for the basketing of subpart F income, typically by looking at what basket of income at the payor the payment reduced. See I.R.C. § 904(d)(3) and Treas. Reg. § 1.904-5.

[4] See also Treas. Reg. § 1.951A-6.

[5] Treas. Reg. §§ 1.960-1(b) and 1.960-2(c).

[6] See Treas. Reg. § 1.861-9T(f)(3).

[1] I.R.C. § 954(b)(3)(B).

[2] This landscape is still very much up in the air. It is expected that Democrats will control the House and Presidency, but the Senate rests on the Georgia Senate runoff election on January 5th.

[1] Prop. Reg. §1.954(c)(6)-2. (REG-110059-20, September 22, 2020)