The C-Suite is the executive leadership team responsible for managing an organization through operational oversight and strategic decision-making. With that comes a significant number of daily decisions that impact the business’s direction. For many companies, these decisions could be the difference between growth, stagnation, and decline. Typically, thoughtful, forward-looking decisions that embrace change fuel growth, whereas comfortable, short-sighted decisions that focus on the status quo can lead to stagnation — if not decline.

However, the difference between a “good” decision and a “bad” one is often narrower than it appears. Outcomes are rarely defined by obvious right-versus-wrong choices, but by subtle nuances in judgment. For example:

- A small piece of missing information

- A minor miscalculation

- An overlooked detail

- A wrong assumption

- A bad estimate or data point

Now, combine the small gap between good and bad decisions with the understanding that every decision carries a tax impact. Often, the subtle nuances in decision-making either begin as tax issues or have downstream tax implications, potentially leading to misstatements, audit findings, regulatory disputes, or control weaknesses. Tax shows up in more places than most leaders expect, which is why it is so widely accepted in C-Suite offices around the world. Corporate tax tends to hide in the wiring of a company.

Unfortunately, when business decisions are made, the impact of tax is often not appropriately and thoughtfully considered. Companies may have the best-laid plan from an X’s-and-O’s perspective regarding legal, accounting, and/or risk, but if tax implications are not considered, the plan could unravel or lead to unintended consequences. Unfortunately, companies often don’t operationalize their strategies or fully understand the impact of tax. Accordingly, there are many areas of operations, strategy, and reporting in which corporate tax is deeply embedded, including:

- Financial Reporting

- Small changes in assumptions can lead to material misstatements.

- Judgments and estimates are very often considered in deferred taxes, valuation allowances, and uncertain tax positions.

- Internal Controls & Systems

- Tax calculations are only as reliable as the underlying financial data and related controls.

- Data used for tax reporting and forecasting comes from many systems, so a lack of integration between teams and significant manual adjustments could create control weaknesses.

- Mergers & Acquisitions

- Many post-deal surprises are typically tax issues (both income and indirect taxes) that weren’t fully understood.

- Tax considerations may help shape the proposed transaction structure, but unexpected tax liabilities identified during due diligence could significantly impact or prevent closing.

- Global Operations

- When operating on a global scale, companies face a range of new tax issues arising from differences in laws, reporting requirements, and enforcement across multiple jurisdictions.

- Errors often arise from documentation gaps, inconsistent assumptions, and reporting discrepancies.

- Market Growth & Expansion

- The tax cost of growth and expansion could be high if not properly analyzed.

- Building a new facility to hold inventory, hiring employees for a new office location, and selling services to new customers can all trigger complex tax rules across the tax landscape (direct and indirect).

- Cash Flow & Treasury

- Tax impacts cash, not just reporting.

- A forecasting error in estimated tax payments, a miscalculation of repatriated foreign earnings, or a tax misclassification of debt and dividends could lead to large, unexpected cash outlays (including interest and penalties) or even liquidity problems.

- Executive Compensation & Incentives

- Misunderstanding tax effects can distort incentives or reported results.

- The tax treatment and timing of payments could have serious implications for both the individual and the business related to bonuses, stock compensation, and other long-term incentive plans.

- Business Structuring Decisions

- How companies are structured and funded is driven by tax rules.

- Tax drives entity classification (corporation, disregarded entity, partnership), capital financing (cash, debt, equity), and inter-company relationships (management fees, pricing of goods and services, financing options).

- Legal & Regulatory Risk

- Risk management tolerance influences tax positions taken.

- Tax positions can be challenged by taxing authorities or financial statement auditors, disclosed in tax returns or regulatory documents, and subject to penalties for aggressive interpretations or controversial conclusions.

Although many companies that sell similar products or services may seem alike at a surface level, a deeper analysis of their “hard-wiring” typically uncovers substantial differences, especially in the tax area. No two companies have the same tax profile, even when they have the exact same footprint. A company’s tax profile is a complex web of decisions, positions, and interpretations. Some companies use a methodical, systematic, and thoughtful approach to proactively determine their tax profile, whereas others take a haphazard approach.

Unfortunately, many companies make tax decisions by the seat of their pants, unaware that their strategic and operational decisions carry significant tax implications.

Most executive leaders would agree that it is imperative to prioritize the tax function, but executing that prioritization is not as easy. The number of competing corporate priorities can limit the availability of allocable resources, investment capital, and dedicated time, potentially deprioritizing tax. In the past, many companies followed the old adage, “If it ain’t broke, don’t fix it.” In other words, tax is not a priority until it becomes one.

In an ever-changing tax landscape, the status quo doesn’t work. The tax function is evolving from a compliance-focused model to a strategic one. Yet, for some companies, the change is slow. For the most part, tax professionals understand the prioritization hierarchy within the corporate structure, but they are also working harder than ever to explain to executive leadership that tax is deeply embedded across many areas of corporate operations, strategy, and reporting.

Ultimately, for a business to have long-term success, executive leaders need to invite tax to the decision-making table to align the tax function with the overall business goals and objectives. Such an invitation suggests that executive leadership wants the tax function to have an influential voice and a consistent, open line of communication with decision-makers. The manner in which this influence is exercised is shaped by the C-Suite’s five key decision points — Strategic Tilt, Governance, Integration, Technology, and Staffing — as outlined in a previous blog.

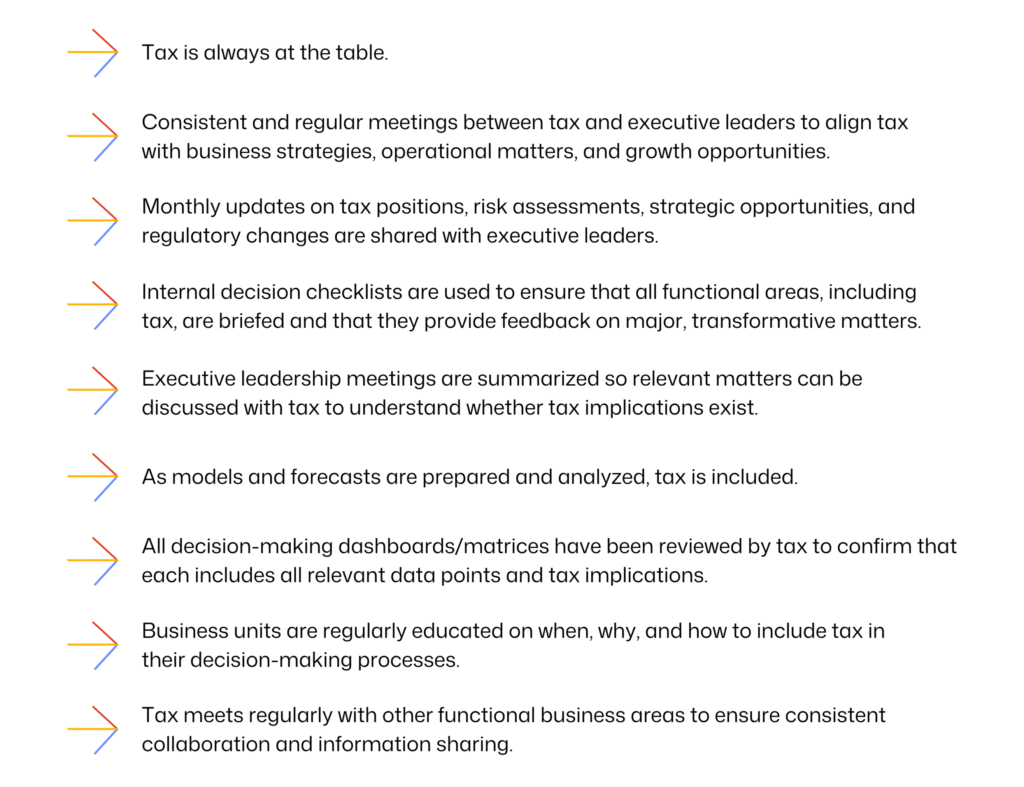

There are many ways for executive leaders to support the tax function’s climb up the hierarchy by simply modifying certain corporate behaviors that shouldn’t entail a high cost (in terms of resources, money, or time). Below are some simple examples:

In today’s complex and rapidly evolving business environment, tax should no longer be a back-office compliance function. It needs to be an integral part of how companies operate, grow, and manage risk. The difference between a well-executed strategy and one that unravels often lies in small, easily overlooked details, many of which have tax implications hiding beneath the surface. When tax is excluded from decision‑making, even well‑intentioned business strategies can produce unintended consequences that impact cash flow, financial reporting, reputational risk, and long‑term value.

Successful companies recognize that tax should inform decisions without dictating them. Every company must define its own approach to the tax function. In a landscape where the margin between good and bad decisions is razor-thin, prioritizing tax can be the difference between momentum and a misstep.