Choosing the right staffing approach, among insourcing, co-sourcing, or outsourcing, for a corporate tax function is one of the most important structural decisions a C-Suite can make with respect to aligning tax with the rest of the company’s goals and objectives.

This article addresses the staffing question directly — the practical choice between building capability internally, partnering externally, or combining both. The answer shapes every prior decision: how the tax function is aligned, how it becomes a priority, and how it collaborates across the business.

Generally, most people assume that tax work is done in-house, with external advisors brought in for specific transactions or technical opinions. The expansion of managed services practice lines within large accounting firms, together with the growth of boutique consulting firms, made external delivery more capable and cost-effective than ever before. This shift, combined with the broader acceptance of outsourcing as a legitimate strategic choice, opened the door to more fundamental questions about who should be doing the work. Technology, particularly cloud-based tax platforms, automated compliance tools, and data analytics, has further accelerated this, making it easier for external providers to deliver high-quality tax services without being physically embedded within the company.

This outward shift did not stop at full outsourcing. The same pressures that pushed work externally — escalating regulatory complexity, a shrinking pool of experienced tax professionals, tighter budgets, and the rising cost of keeping technology current —intensified further, while global reforms such as the OECD’s Pillar Two added a new layer of demand for specialists. Many companies that handed the entire function to an outside provider often found they had traded one problem for another, giving up the control, transparency, and institutional knowledge that come with doing the work in-house. Co-sourcing emerged as the answer: A third party works alongside the internal team in defined areas, preserving oversight while still providing scale and specialist expertise.

The data reflects this shift. In EY’s 2024 Tax and Finance Operations survey[1], 54% of tax leaders said they were rethinking their operating model, and co-sourcing was the most commonly cited change. The question is no longer whether outsourcing or co-sourcing the tax function is acceptable; now, it is simply which approach is right for a company at a given point in its development.

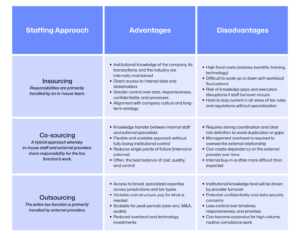

Before getting too deep into the optimal staffing approach, it’s best to first understand the advantages and disadvantages of each. Weighing these advantages and disadvantages up front allows a company to align its approach with what it values, rather than defaulting to what is familiar or simply the cheapest. It also frames the six factors that follow, since each factor is really a question of which trade-offs a company can most afford to make.

There is no universally correct approach, and the decision is rarely straightforward. Each approach carries real trade-offs, and none is without some sacrifice. An approach that looks attractive on cost may give up control, continuity, or institutional knowledge, while the most controlled option may prove too rigid or expensive to sustain. The right staffing model depends on a combination of factors, including the company’s size, geographic footprint, strategic priorities, and the experience of its existing team. For some companies, the answer is clear; for others, it requires careful consideration, given the significant impact that the choice will have on the people, processes, and governance of the tax function.

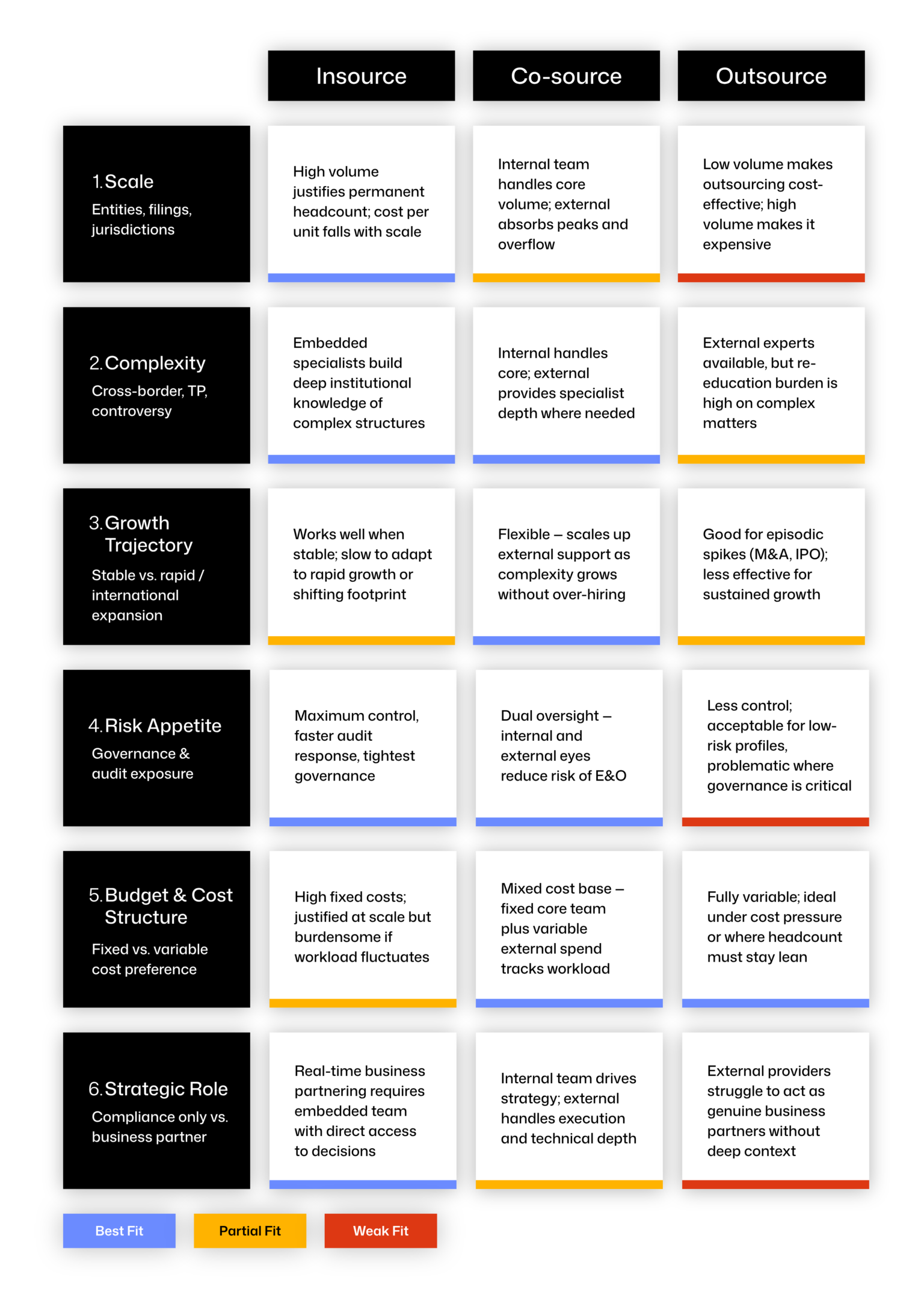

Generally, six factors drive the decision, but they don’t carry equal weight. Two of them, scale and complexity, set a company’s baseline approach: Scale drives the economics, with outsourcing cheaper per unit at low volume and in-house more cost-effective at high volume, while complexity drives the need for specialization. The other four, growth trajectory, risk appetite, budget, and strategic role, then shift that baseline in a particular direction.

Certain combinations point strongly toward a single approach, as the grid below shows.

Co-sourcing is the most versatile approach because it blends the strengths of the other two. Insourcing is preferable based on the typical factors that matter most to large, complex, strategically driven functions (risk, strategic role, complexity). Outsourcing is a strong fit in cost-conscious, low-volume situations, but a weak fit wherever control, governance, or strategic partnering matters.

If mapped onto two axes, scale and complexity, most companies fall into one of four quadrants:

- Low scale, low complexity — outsource is almost always right

- Ex: Mid-Market manufacturers with straightforward US compliance needs

- Low scale, high complexity — co-source or targeted outsource of specialist areas

- Ex: Growth stage life sciences with large R&D expenditures and emerging market issues

- High scale, low complexity — insource for efficiency

- Ex: Large mature national retailer with a high volume of repeatable tasks

- High scale, high complexity — insource core, co-source or outsource specialist areas

- Ex: Large multinational industrial / life sciences / etc.

Within each quadrant, those other four factors pull the approach in a specific direction:

- A high-growth company moves toward co-sourcing even if its current scale is low

- A low-risk appetite moves toward insourcing even if scale doesn’t fully justify it

- A tight budget moves toward outsourcing, even if the complexity is high

- A strategic tax role expectation moves toward insourcing regardless of scale

Obviously, as a company’s direction changes, so should its staffing approach. Accordingly, the most effective leaders treat their staffing approach as fluid, reassessing it regularly against the company’s current size, strategy, risk profile, and budget, rather than adopting a fixed approach.

Below are some typical examples of events in which companies reevaluate their approach in fulfilling the roles and responsibilities of the tax function:

Understanding the trade-offs is necessary — but knowing which trade-offs apply to your company requires a more deliberate assessment.

The companies that get this right don’t pick the most popular model — they audit their own situation honestly (cost structure, risk exposure, growth ambition) and treat staffing as a living choice, not a one-time decision.