When people think of a company, they often focus on its products or services, overlooking the many business functions that make its success possible. Like a sports team, no single role is more important than another — each function contributes unique value, and works together to build, manage, and operate the business.

Behind the scenes, teams across a company bring expertise, accountability, and shared purpose. Ultimately, strong collaboration and clear communication are what unify their efforts and drive sustained success, whereas a single function lacks the information or expertise needed to run a business effectively. When teams share insights and stay aligned, decisions are more informed, problems are solved faster, and work moves forward without costly misunderstandings or duplication.

They also create consistency and trust across the company. Clear communication ensures everyone works toward the same goals, while collaboration brings together diverse perspectives to drive better outcomes, especially in complex or fast-changing environments.

Companies typically have a variety of functional areas that are responsible for the success of the business. While the specific structure of each area varies by industry and size, most corporations include the following:

Within each of these functional areas are broader domains that require extensive experience and technical expertise to deliver meaningful value to the company. Although the tax function typically resides within finance and accounting, it needs to collaborate with each of these functional areas as tax touches virtually every aspect of a company. As discussed in Part 1 of this series, many organizations still face a disconnect between recognizing the strategic importance of tax and meaningfully involving tax leaders in broader business decisions. Decisions made across the organization can have significant and sometimes unexpected consequences. Without proactive collaboration, those consequences often go unrecognized until it is too late to mitigate them.

While collaboration across the entire company is important, the relationship between tax and the broader finance and accounting function is uniquely critical. Finance and accounting serve as the financial backbone of the company, and, as described below, tax is deeply intertwined with virtually every process, system, and output produced by each of the broader domains within the finance and accounting function.

Accounting & Financial Reporting

Focus Area – Records financial results and ensures accuracy, compliance, and audit readiness.

This is perhaps the most foundational collaboration for tax. The tax function relies on accurate, timely financial data from accounting to prepare filings, calculate tax provisions, and support audit requirements. Equally, accounting depends on tax to ensure that deferred tax assets and liabilities, uncertain tax positions, and current tax expenses are properly recorded in the financial statements. Close coordination during the monthly and quarterly close process is essential to avoid errors and ensure compliance with applicable accounting standards.

Financial Planning & Analysis (FP&A)

Focus Area – Budgeting, forecasting, and performance analysis to support leadership decision-making.

Tax and FP&A must work closely to ensure that tax costs are accurately reflected in budgets, forecasts, and financial models. Tax should provide FP&A with reliable, effective tax rate estimates, anticipated cash tax payments, and visibility into any tax planning initiatives that could impact financial performance. In turn, FP&A should engage the tax team early when modeling new business scenarios, growth investments, or structural changes, as these decisions almost always carry tax consequences that can materially affect the numbers.

Treasury

Focus Area – Manages cash, liquidity, and financial risk across banking, financing, and market exposures.

Tax and treasury intersect frequently, particularly around cash repatriation, intercompany funding structures, and debt financing. Beyond these strategic considerations, tax also has a direct impact on the day-to-day treasury function, as income, franchise, gross receipts, sales and use, and other taxes can significantly affect a company’s daily cash inflows and outflows. Tax needs visibility into the treasury’s cash flow plans and financing arrangements to identify withholding tax obligations, assess the tax efficiency of capital structures, and ensure intercompany loans are properly priced and documented. Treasury, in turn, benefits from tax input when evaluating the after-tax cost of financing options and managing cash across multiple jurisdictions.

Internal Audit

Focus Area – Evaluates internal controls and risk processes to promote efficiency and mitigate compliance risks.

Tax should collaborate with internal audit to ensure that tax controls, processes, and compliance procedures are subject to regular review. Internal audit can provide an independent assessment of whether tax risks are being appropriately identified and managed, while tax can help internal audit understand the regulatory landscape and flag areas of risk. A strong relationship here supports the broader governance framework and helps the company stay ahead of potential issues before they become material.

Risk Management

Focus Area – Identifies and mitigates financial and operational risks across the organization.

Tax is one of the most significant risk areas within any company, and includes evolving regulatory changes, nexus determinations, transfer pricing arrangements, audit exposures, and reputational risks associated with aggressive tax positions or errors in the reporting process. Tax should work with risk management to ensure tax risks are properly captured within the company’s risk framework and that mitigation strategies are in place. Risk management should also engage tax when evaluating structures, indemnification arrangements, and other transactions and agreements that may have tax implications.

Investor Relations (IR)

Focus Area – Communicates financial performance and strategy to shareholders and analysts.

Tax plays an important supporting role for IR, particularly when communicating the company’s effective tax rate, tax strategy, and material tax developments to investors and analysts. This becomes especially critical during periods of tax law changes or material transactions, when investor scrutiny tends to increase. Organizations must be prepared to address detailed questions during earnings releases and related Q&A discussions. As stakeholders increasingly scrutinize corporate tax practices, IR and tax must be aligned on messaging to ensure transparency, accuracy, and consistency across the organization. Tax should also be consulted when preparing earnings releases, investor presentations, or responses to analyst questions that touch on tax matters.

Procurement

Focus Area – Manages sourcing and purchasing with a focus on cost control and supplier management.

The intersection of tax and procurement is often underestimated or overlooked entirely. Tax needs to collaborate with procurement to ensure that vendor contracts properly address tax obligations, including sales and use tax, VAT, and withholding tax. Procurement should engage tax early in the supplier selection and contract negotiation process, particularly for cross-border transactions, where the tax treatment can significantly affect the true cost of goods and services.

Corporate Development

Focus Area – Drives strategic growth through acquisitions, divestitures, and partnerships.

This is one of the most critical and time-sensitive collaborations for tax. Mergers, acquisitions, divestitures, and restructurings all carry significant tax consequences that can directly affect value and organic growth decisions. Tax must be integrated into the due diligence process from the outset to identify historical tax liabilities, assess the tax efficiency of deal structures, and evaluate post-transaction integration considerations. A tax perspective brought in too late can result in missed opportunities or, worse, unforeseen liabilities that erode the value of a transaction.

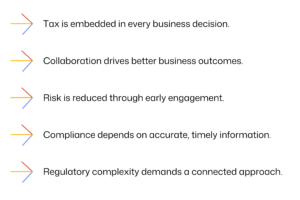

As outlined above, there are several reasons why cross-functional collaboration with the tax function is essential for a company to meet its business goals and strategic objectives: In short, a tax function operating in isolation is always playing catch-up. Collaboration is not just a best practice; it is a strategic necessity. Companies that recognize this and invest in breaking down the silos surrounding tax will be better positioned to manage risk, optimize their tax position, and drive long-term value — turning a back-office function into a strategic asset.

In short, a tax function operating in isolation is always playing catch-up. Collaboration is not just a best practice; it is a strategic necessity. Companies that recognize this and invest in breaking down the silos surrounding tax will be better positioned to manage risk, optimize their tax position, and drive long-term value — turning a back-office function into a strategic asset.